About exactly one year ago, I sat on the edge of my bed, staring blankly at the ceiling, feeling a crushing weight sitting right in the middle of my chest.

I had just checked my bank account balance. It was the twenty-eighth of the month, payday was still three days away, and I had exactly fourteen dollars and thirty-two cents to my name.

I was not unemployed. I was making a decent salary. Yet, every single month, I was riding the exact same terrifying rollercoaster. The money would arrive in my account, I would feel a brief, intoxicating wave of wealth, and then, completely inexplicably, it would vanish into thin air.

I was living paycheck to paycheck, not because I wasn’t earning enough, but because I had absolutely zero visibility into my own behavior.

I realized that night that sheer willpower was never going to fix my finances. Willpower is fragile. It breaks when you are tired, hungry, or stressed out from work. I didn’t need to try harder; I needed to build a digital fence around my money. I needed systems that were smarter and more disciplined than my own impulses.

I spent the next twelve months treating my smartphone like a financial advisor. I downloaded, tested, and integrated a massive array of software into my daily life. If you are tired of the end-of-the-month panic, here are the 11 finance apps that completely transformed my relationship with money and helped me save thousands this year.

(Disclaimer: I am not a financial advisor, and this is not professional financial advice. This is simply the story of the tools that repaired my personal financial life.)

1. YNAB (You Need A Budget): The Absolute Game Changer

If I had to delete every single app on my phone and only keep one, it would be YNAB.

Before YNAB, I practiced what is known as “forecasting.” I would look at my expected paycheck, guess what my bills would be, and hope the math worked out. It never did.

When I first sat down to figure out (How to Budget Your Money With a Finance App), YNAB forced me into a completely different paradigm: Zero-Based Budgeting. The app only lets you budget the money that is physically sitting in your bank account right this second. You cannot budget next week’s paycheck.

It forces you to give every single dollar a specific “job.” When my paycheck hits, I go into the app and assign money to my rent category, my groceries category, and my emergency fund. When the money hits zero, I stop assigning.

It completely eliminated the anxiety of wondering if I could afford something. If there is money in the “Dining Out” category, I can buy the pizza guilt-free. If the category is empty, I eat leftovers. YNAB didn’t just track my money; it actively changed my psychology.

2. Rocket Money: The Subscription Slayer

We are living in the golden age of the “convenience tax.” Everything is a subscription, and companies rely entirely on human forgetfulness to keep their revenue flowing.

I thought I had a pretty good handle on my monthly bills. Then I downloaded Rocket Money and synced it to my credit card.

The app scanned my transaction history and presented me with a horrifying, categorized list of my recurring charges. I was paying for a premium streaming service I hadn’t watched in eight months. I was paying $12 a month for a digital magazine I never opened. I was still paying for a specialized fitness app from a New Year’s resolution two years ago.

In exactly fifteen minutes, I went down the list and hit “Cancel” on over $75 worth of monthly ghost subscriptions. That is $900 a year put straight back into my pocket, all because an app illuminated the blind spots in my spending.

3. Oportun (formerly Digit): The Invisible Savings Bot

I am notoriously bad at manually transferring money into my savings account. If I see the money sitting in my checking account, my brain automatically assumes it is there to be spent.

Oportun acts as a silent, invisible financial assistant that lives in the background of your bank account.

The app uses an algorithm to study your spending habits, your upcoming bills, and your cash flow. Once it understands your baseline, it starts secretly skimming tiny, insignificant amounts of money out of your checking account and moving it into a secure savings vault.

It might move $2.40 on a Tuesday, and $5.10 on a Thursday. You never notice the money is gone because the amounts are so small. But after three months of doing absolutely nothing, I opened the app and found almost $400 sitting in my digital vault. It is the ultimate tool for people who struggle with the discipline of manual saving.

4. Acorns: Weaponizing My Coffee Habit

I buy a lot of coffee. It is my one true vice. In the past, every time I swiped my card for a $4.50 latte, I felt a tiny pang of financial guilt.

Acorns completely flipped that dynamic by weaponizing my daily purchases into an investment strategy through “round-ups.”

Whenever I buy that $4.50 coffee, Acorns automatically rounds the purchase up to the nearest whole dollar. It takes that extra $0.50 and funnels it directly into an automated, diversified investment portfolio.

It sounds trivial, but those micro-investments compound. Every time I bought groceries, bought gas, or paid for parking, spare change was quietly being invested in the stock market. Over the course of the year, those round-ups accumulated into a surprisingly robust emergency fund. It turned the simple act of spending into a mechanism for saving.

5. Splitwise: The Friendship Preserver

If you frequently travel with friends, go out to group dinners, or live with roommates, you are probably losing money simply because you feel too awkward to ask for it back.

I was the person who always put my credit card down for the table, assuming everyone would Venmo me later. Half the time, people forgot, and I felt too petty to send a reminder text over $14. I was quietly bleeding hundreds of dollars a year subsidizing my social life.

Splitwise removed all the emotion from group expenses.

Now, when I buy the concert tickets, I immediately log the receipt into Splitwise. The app tracks who owes what, keeps a running tally, and sends automated push notifications to the group to settle up at the end of the month. It acts as an objective, neutral debt collector, saving my money and preserving my friendships.

6. Fetch Rewards: Gamifying the Grocery Run

Groceries are one of my largest variable expenses, and with recent inflation, the checkout line had become a source of major anxiety.

I don’t have the patience to sit at my kitchen table and clip physical coupons for hours. Fetch Rewards provided the perfect, low-friction alternative.

After I get home from the supermarket, I take my physical receipt, open the app, and snap a quick photo of it. That’s it. The app scans the receipt and awards me points based on the brands I purchased.

Once you accumulate enough points, you can instantly cash them out for digital gift cards. I use the app religiously to fund my Amazon purchases. It doesn’t require any pre-planning or altering of my shopping lists; it just gives me free money for taking a five-second photograph of a piece of paper I was going to throw away anyway.

7. Wise (formerly TransferWise): The International Lifesaver

A significant portion of my financial waste used to happen when I traveled internationally or bought software from overseas vendors.

Traditional banks are predatory when it comes to foreign transaction fees and bloated exchange rates. Every time I swiped my local debit card in a foreign country, I was getting hit with an invisible 3% to 5% tax.

Opening an account with Wise completely eliminated this drain.

The Wise app allows me to hold dozens of different currencies in one single digital wallet. When the exchange rate for the Euro drops, I can transfer money from my local currency into my Euro wallet instantly, locking in the good rate. When I use their physical debit card abroad, it pulls directly from the local currency wallet with zero hidden fees.

If you do any sort of international spending, holding a multi-currency digital wallet is absolutely essential for plugging those expensive, hidden leaks.

8. Monarch Money: The Holistic Dashboard

While YNAB is fantastic for day-to-day budgeting, I eventually needed a tool to look at the macro picture of my financial health. I wanted to see my net worth, my retirement accounts, and my daily spending all in one unified dashboard.

This pursuit of macro-level tracking was a turning point. It made me realize that to stay sane, you have to organize your data effectively, a concept I explored deeply in my piece on (Tricks to Use Finance Apps Without Stress). If your data is fragmented, you will panic.

Monarch Money became my financial command center.

It connects to everything: my checking accounts, my credit cards, my investment portfolios, and even the estimated value of my car. It provides stunning, easy-to-read graphs of where my wealth is distributed. Seeing my net worth slowly tick upward month by month provided a massive psychological boost. It gave me the long-term motivation I needed to stick to my short-term budget.

9. Honey (Browser Extension & App): The Impulse Control Mechanism

A huge chunk of my disposable income used to disappear into the void of online shopping. I would get targeted by an Instagram ad, click the link, and buy a shirt within three minutes.

Installing the Honey app and browser extension introduced a crucial layer of friction, alongside a mechanism for immediate savings.

When I get to a digital checkout page, Honey automatically scours the internet for promo codes and tests them in real-time. It ensures I never pay full price if a discount exists.

But more importantly, it has a feature called the “Droplist.” If I see an expensive pair of headphones I want, instead of buying them, I add them to my Droplist. Honey tracks the price of that item across the web. Usually, within a few weeks, the price drops, and the app alerts me.

This taught me the power of delayed gratification. Nine times out of ten, by the time the price drops two weeks later, the emotional urge to buy the item has completely passed, and I save 100% of the money by simply closing the tab.

10. Goodbudget: The Digital Envelope System

Before the digital age, people used to manage their finances using physical envelopes of cash. You put $200 in the “Groceries” envelope, and when the envelope was empty, you stopped buying groceries. It is an incredibly effective, tactile way to control spending.

Goodbudget brings this exact philosophy to your smartphone.

For a brief period this year, my expenses were incredibly tight, and I needed an aggressively visual way to stop myself from overspending. I went into immense detail about this specific struggle in my article on (The Budgeting App That Helped Me Finally Save Money).

Goodbudget doesn’t sync directly to your bank accounts, which is actually its greatest strength. It requires you to manually input your transactions. Every time I spent money, I had to open the app, type in the amount, and watch the visual “envelope” empty out on my screen.

That physical friction of having to manually log the expense made me hyper-aware of every single swipe of my card. It is the perfect app for financial rehabilitation.

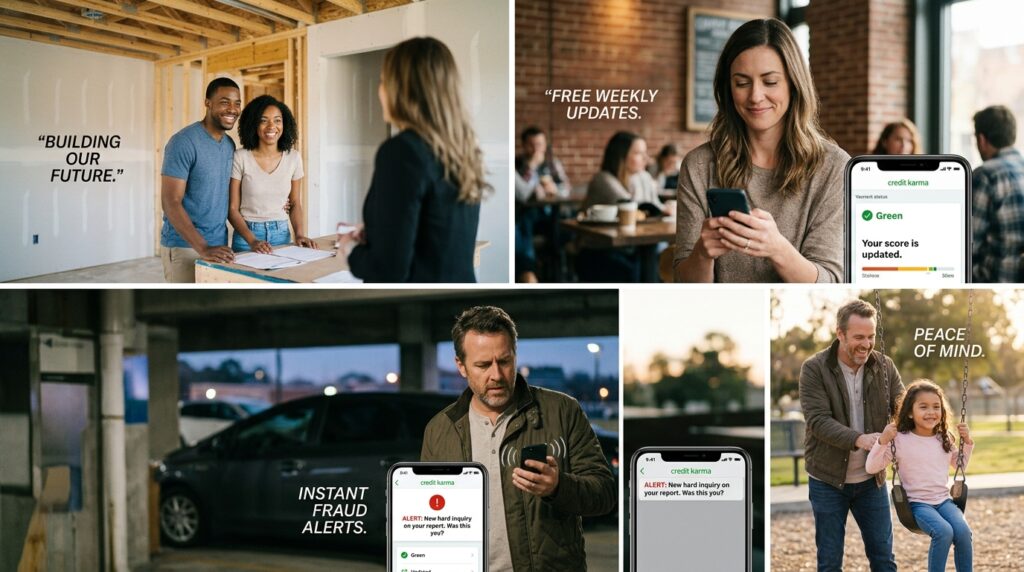

11. Credit Karma: The Defensive Shield

Finally, saving money isn’t just about cutting expenses today; it is about protecting your financial reputation for tomorrow.

Your credit score dictates the interest rate you get on your car loan, your mortgage, and even affects your ability to rent an apartment. A bad credit score will cost you tens of thousands of dollars over the course of your life.

I used to be terrified of checking my credit score. It felt like stepping on a scale after the holidays.

Credit Karma changed that. It provides free, weekly updates to your credit profile, but more importantly, it monitors your identity. If a new credit card is opened in my name, or if a hard inquiry is pulled on my credit report, the app sends me an instant push notification.

Knowing that my financial identity is actively being guarded by an algorithmic watchtower gives me immense peace of mind. It allows me to catch errors and potential fraud before they have a chance to drain my actual bank accounts.

Final Thoughts on Financial Sovereignty

Looking back at the person I was a year ago—sitting on the edge of the bed, paralyzed by the stress of fourteen dollars in checking—I hardly recognize myself.

The transformation didn’t happen because I won the lottery. It didn’t happen because I suddenly developed ironclad willpower. It happened because I swallowed my pride, admitted my systems were broken, and allowed technology to act as my financial guardrails.

Money is not inherently evil, and it is not a mysterious force. Money is simply data.

When you don’t track your data, it controls you. It causes panic, arguments, and sleepless nights. But the moment you download the right tools, connect your accounts, and force the data into the light, everything changes.

You stop wondering where your money went, and you start actively telling it where to go.

If you are feeling overwhelmed by your finances right now, pick just one app from this list. Start with finding your ghost subscriptions, or set up an automated savings bot. Take one tiny digital step today, and I promise you, by this time next year, your entire financial reality will look completely different.